Episode 5 - ATM King: Royally Screwed

ATM King: Royally Screwed

Episode 5

Parallels of a Ponzi

Overview

Imagine a business so brilliant, it practically prints money! The pitch is simple: passive income, steady returns, and machines that never sleep. But behind the glossy promises lurks a familiar deception, one perfected over a century ago by a man named Ponzi and now dressed up in modern tech and small-town charm. This is a story about how the numbers stop adding up and how a scheme stitched together with bold promises and borrowed time eventually unravels, leaving nothing but questions, empty accounts, and a trail of financial wreckage.

The year was 1920, and in Boston, Massachusetts, Charles Ponzi had stumbled upon what he called the "opportunity of a lifetime." His plan revolved around international postal reply coupons, which allowed senders to prepay postage for recipients in other countries. Ponzi claimed he could exploit currency fluctuations by purchasing cheap coupons in Europe, redeeming them for stamps in the U.S., and selling those stamps for a hefty profit.

But the true brilliance of Ponzi’s scheme was in its marketing. He promised investors a 50% return in just 45 days or double their investment in 90 days. It was irresistible. Investors flooded him with cash, convinced they’d struck gold. What they didn’t know was that Ponzi wasn’t buying or selling postal coupons at all. Instead, he was using new investors’ money to pay returns to earlier ones.

Charles Ponzi - from Jared Enos/CreativeCommons

For example, if one investor put in $100, Ponzi might pay them $150, by taking that $150 from two new investors. Those two new investors would then be paid with money from four more recruits. The cycle only worked as long as new people kept joining.

At its peak, Ponzi was raking in millions per week. He lived lavishly, mansions, expensive suits, fine cars. But as journalists and investigators began asking questions, the house of cards collapsed. By the time the dust settled, Ponzi had swindled thousands out of $20 million, nearly $300 million in our time.

A Ponzi Scenario: Get Out Your Calculators

Before continuing, it is important to understand that there is no absolute proof that the Heller/Paramount ATM scheme was a Ponzi. When the criminal case plays out, we’ll be able to see exactly what was happening with the investor money. For the sake of legality, we are going to develop a scenario that follows the Ponzi structure and apply the features of the Paramount case to it.

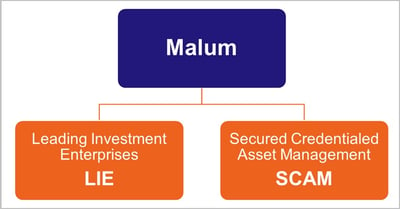

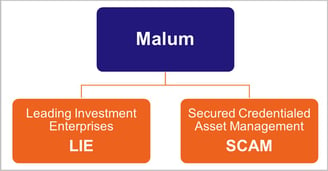

Meet Malum, a businessman with a golden pitch. In 2019, Malum established two companies: Leading Investment Enterprises (LIE), which sells and manages ATM funds, and Secured Credentialed Asset Management (SCAM), who provide all of the ATM management services for the network to function. His goal: selling investors on the idea of owning ATMs - a passive income stream that will generate consistent, high returns.

We’ll scale down the scheme and standardize it to keep it simple. Here’s the pitch:

Purchase an ATM from SCAM for $15,000 through Malum’s investment group LIE.

LIE will pay SCAM to purchase ATMS, then SCAM will do all the rest! Within three months, they’ll place the ATMs, get all the contracts signed, keep it filled, and collect all the revenues. 25% of the monthly transaction fees will be sent to LIE, who will then send the investor a monthly check.

LIE will send the investor a check for $300 every month for 84 months for a total of $25,200. The investor will have an overall profit of $10,200 at the end of the term.

Step 1: The Birth of a Scam

Malum used his reputation and community connections to lure in early investors. Many were members of tight-knit religious communities, where trust is built on word-of-mouth, not financial audits. Through personal pitches and formal investment meetings, Leading Investment Enterprises (LIE) sold 50 ATMs, taking in $750,000 from mostly friends and family.

In the normal business world, LIE would have then purchased 50 machines from Secured Credentialed Asset Management (SCAM). SCAM would obtain 50 machines, place them at various locations, and send documentation of the purchases, agreements, machine information, and location back to LIE to share with the investors.

But Malum was no ordinary businessman. Prior to purchasing the ATMs, LIE took 25% of the investor’s money for “expenses” and other work involved in preparing and managing the Fund. Then, LIE purchased five (5) ATMs from SCAM at a cost of $8,000 apiece. SCAM also charged LIE a fee of 10% of the total purchase amount for every Fund. Over a third of investor money had gone to various “expenses.”

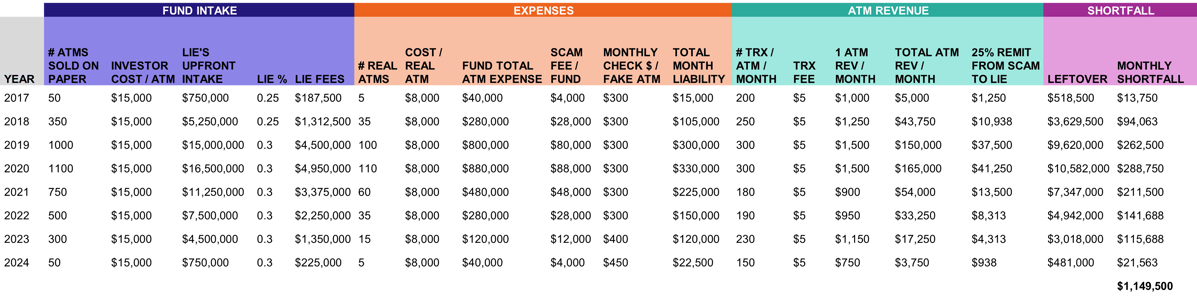

Step 2: Attracting the First Investors (2017)

Investment Inflow

$750,000 was raised from 50 investments.

Expenses

$40,000 was spent on legitimate ATM purchases.

LIE has a monthly liability of $15,000 to its investors.

LIE charged the investors $187,500 for Fund management expenses.

SCAM charged LIE $4,000 for ATM purchase-related fees.

ATM Revenue

The 5 legitimate ATMs take in $5,000 in overall revenue each month. As contracted, $1,250 per month (25%) is sent from SCAM to LIE for the investors’ monthly checks.

Revenue Shortfall

Malum’s ATMs cannot cover the monthly check liability of $15,000; in fact, he will need to cover $13,750 out-of-pocket each month.

Only $518,500 of investor money was left after expenses, meaning that monthly payments will only last for 38 of the contracted 84 months.

Each investor will lose about $3,700 of their upfront money along with any guaranteed profit unless action is taken.

There aren’t a lot of options for Malum now that he has started the scheme. There isn’t enough money to get on a plane and escape reality, so he must get more investors and Funds organized.

From the initial $750,000 investment, Malum's investment company LIE will take 25%

The purchased of 5 real ATMs cost Malum's ATM group, SCAM, $40,000. SCAM also added a 10% fee to the $40,000 for their services. Malum must now start payments of $15,000 per month to his investors in this round.

The 5 ATMs average 200 transactions each month, resulting in $1,250 revenue that will be sent from SCAM to LIE, and eventually investors.

Not including monthly payments, expenses and fees have left Malum with only $518k of cash. Since the ATM revenue cannot support the monthly payment, the remaining investor pool of money must be used to make monthly payments.

Click on image for full-screen view

To keep up the illusion of success, Malum used new investor funds to pay old investors. Happy investors spread the word, and Malum created a larger investment opportunity in January 2018. In this Fund, Malum sold 350 ATMs using the same pitch and terms as before. This time, he purchased 35 legitimate ATMs which were placed in higher traffic locations than the previous year’s machines. Charging $5 per transaction, they average 250 transactions per month.

Step 3: Building Credibility (2018)

Investment Inflow

$5,250,000 was raised from 350 investments.

Expenses

$280,000 was spent on legitimate ATM purchases.

LIE has an updated monthly liability of $120,000 to its investors.

$1.3 million of investor money has to LIE & SCAM fees

ATM Revenue

This year’s legitimate ATMs will take in about $43,750 per month, with just under $11,000 (25%) being sent from SCAM to LIE for the investors’ monthly checks.

Revenue Shortfall

As before, the ATM revenue cannot keep up with the promised monthly payments. Legitimate ATM revenue is short by $107,000 per month.

Approximately $4 million of investor money is leftover, which means that Malum was successful in kicking the can down the road another year. There are 38-39 months of payments that Malum could make before having to make some tough decisions.

Confident that he could keep the scheme going, Malum went all-in to organize two more Funds over the next couple of years. To expand his reach beyond word-of-mouth and some online promotions, Malum connected with a well-renowned salesman named Fraus. Like Malum, Fraus himself came from an insulated, vulnerable community that to this day relies on a man’s word when making deals. As another Fund manager was added, LIE increased its investor fees to 30%. Fraus became an integral part of the LIE family, quickly rising to Vice-President.

In this massive growth phase, LIE sold 2,100 ATMs to investors, however, they only purchased 210 machines from SCAM. These ATMs averaged 300 transactions per month at about $5 per transaction.

Step 4: The Great Expansion (2019 - 2020)

Investment Inflow

Over $31 million was invested in these two years.

Expenses

$1,680,000 was spent on legitimate ATM purchases.

LIE has an updated monthly liability of $750,000 to its investors.

$9.5 million of this Fund’s investor money went to LIE and SCAM expenses.

ATM Revenue

Total legitimate ATM revenue averages $364,000 per month, meaning that $91,000 is sent to LIE for investor checks.

Revenue Shortfall

Cumulative ATM revenue greatly lags behind monthly liabilities by $660,000 each month.

Approximately $17.7 million of investor money is leftover after paying years of liability out of pocket. However, the increased liability has significantly reduced the amount of time this scheme will work.

At this point of the scheme, money will run out in just 26 months. Drastic action must take place to get new investors or other sources of income!

All good things must come to an end, and for Malum and Fraus, they’ll have to scramble to keep investors from asking too many uncomfortable questions. A pandemic greatly impacted most industries, including ATMs. Fewer travelers and drastically increased work from home arrangements meant reduced monthly transactions. Massive layoffs and unpredictable futures left investors leery of putting their disposable cash into assets. Some of Malum and Fraus’ investors started asking questions about the legitimacy of the whole operations, noticing that numbers on statements aren’t adding up and an inability to locate their supposed ATMs.

In a show of desperation, LIE began to sweeten the deal for investors. Instead of being guaranteed the standard $300 per month for every ATM they owned, new ATM purchases would pay between $400 and $450 per month! And the new ATMs weren’t just ordinary ATMs, these were state-of-the-art mini-banking centers that would eventually replace brick-and-mortar banks and revolutionize the industry.

Despite their efforts, Malum and Fraus only sold 1,600 more ATMs. In an attempt to extract as much cash as possible to pay previously liabilities, LIE only purchased 115 ATMs from SCAM.

Step 5: The Collapse of LIE and SCAM (2021-2024)

Investment Inflow

$24 million of investor money was taken in during these four years.

Expenses

$920,000 was spent on legitimate ATM purchases.

After organizing the 2024 Fund, LIE had a monthly liability of $1,252,500.

$7.292 million of this Fund’s investor money went to LIE and SCAM expenses.

ATM Revenue

Total legitimate ATM revenue averages $467,000 per month, meaning that $117,000 is sent to LIE for investor checks.

Revenue Shortfall

ATM revenue can only keep up with approximately 10% of the monthly liability. LIE must pay approximately $1.1 million out-of-pocket to make monthly payments.

Approximately $16 million of investor money is leftover after paying years of liability out of pocket. With a monthly liability of nearly $1.3 million and an ATM revenue shortfall of $1.1 million, the operation will be out of money in a year.

Malum, Fraus, LIE, and SCAM have reached the end. Within a year, there will be no more money to pay the monthly investor liability.

Wrap Up

As we’ve seen, the anatomy of a Ponzi scheme isn’t exactly rocket science: just smoke, mirrors, and a relentless appetite for other people’s money. Missing ATMs, phantom revenue, and manipulated investor statements paint a picture that's hard to ignore. Once the scheme was put in motion, there was no stopping it. Each Fund would simply extend the life of the scheme a little bit longer, but environmental variables along with investor weariness caught up with the schemers as it always does.

But numbers only tell part of the story. Behind every unpaid invoice, every vanished dollar, are real people, families who trusted, invested, and believed. In our next episode, we’ll shift the focus from the impact on paper to the impact on people. You’ll read the detailed accounts of investors whose lives have been upended. These aren’t just statistics; they’re stories of retirements jeopardized, generational land loss, and futures thrown into chaos. And as our Ponzi scenario described, there isn't always just one person running the scheme.

Disclaimer and other information

As these episodes pick up attention, I figured it might be best to document this disclaimer (most Watchdog articles don't get attention outside of our small town):

The author of this blog has no financial interest or investment, personal or familial connection, bone to pick, axe to grind, bellyache, personal vendetta, ulterior motive, or any other wild and/or sordid arrangement, with any of the parties identified or discussed in this series. It's simply personal intrigue at what appears to be a historical financial scandal happening right here in our local communities. I'm not a journalist, make no claims to such, and have no interest in competing with those who provide the news as a career. My goal is simply to provide the information I've compiled through news reports, court documents, social media, and personal contacts with investors in a comprehensive manner that puts all of the pieces together. There's more than just the hot local Prestige v. Paramount case - the numerous creditors filing lawsuits and dozens of our own neighbors losing jobs just before Christmas paint a picture of unbridled greed. <--- Again, you know, that's just, like, my opinion, man.

For another series of news reports, please view the many articles written by LancasterOnline reporters Dan Nephin and Chad Umble. (A paid subscription is necessary to view most articles)